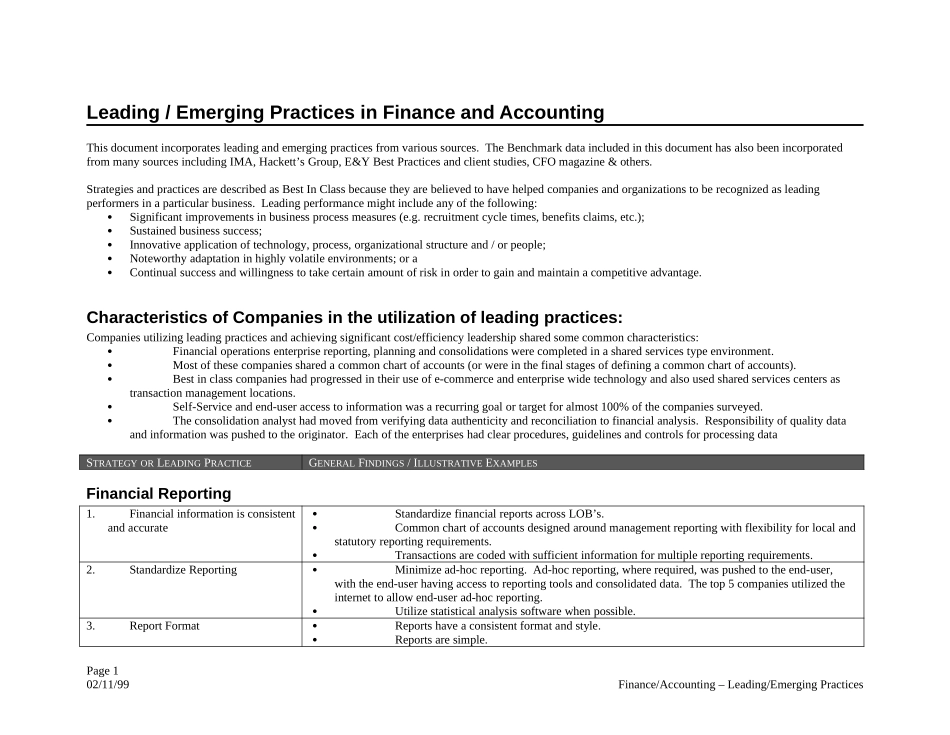

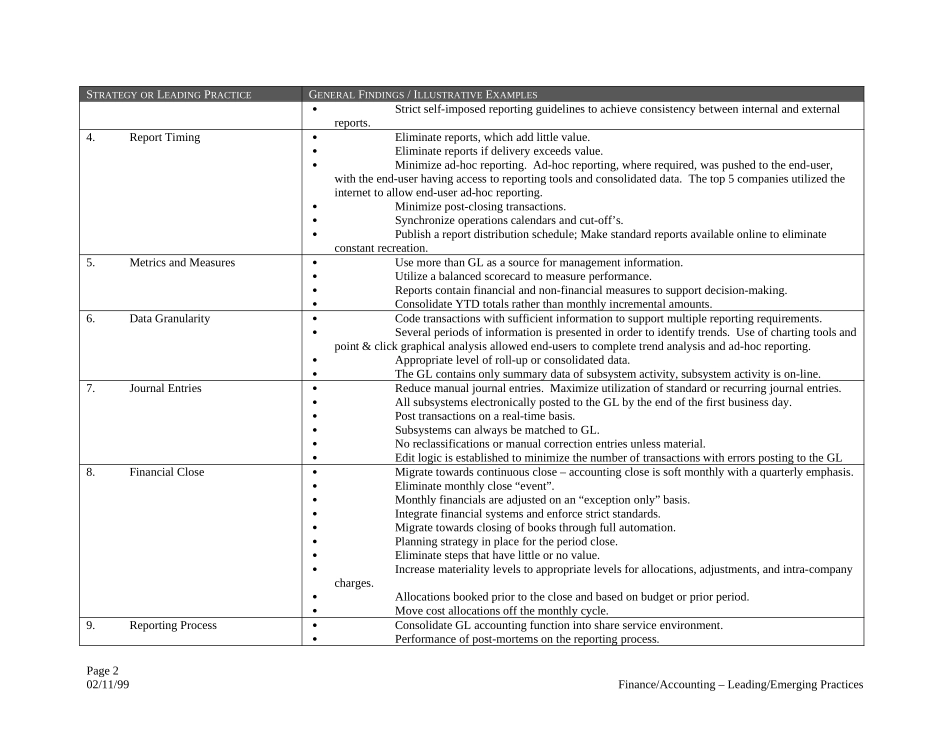

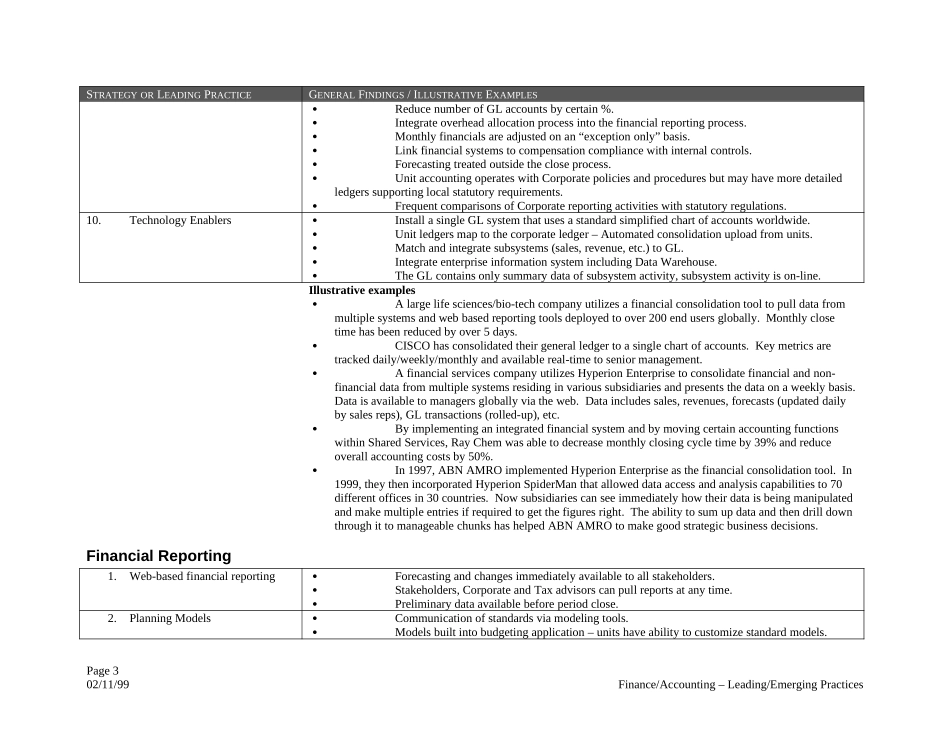

Leading/EmergingPracticesinFinanceandAccountingThisdocumentincorporatesleadingandemergingpracticesfromvarioussources.TheBenchmarkdataincludedinthisdocumenthasalsobeenincorporatedfrommanysourcesincludingIMA,Hackett’sGroup,E&YBestPracticesandclientstudies,CFOmagazine&others.StrategiesandpracticesaredescribedasBestInClassbecausetheyarebelievedtohavehelpedcompaniesandorganizationstoberecognizedasleadingperformersinaparticularbusiness.Leadingperformancemightincludeanyofthefollowing:Significantimprovementsinbusinessprocessmeasures(e.g.recruitmentcycletimes,benefitsclaims,etc.);Sustainedbusinesssuccess;Innovativeapplicationoftechnology,process,organizationalstructureand/orpeople;Noteworthyadaptationinhighlyvolatileenvironments;oraContinualsuccessandwillingnesstotakecertainamountofriskinordertogainandmaintainacompetitiveadvantage.CharacteristicsofCompaniesintheutilizationofleadingpractices:Companiesutilizingleadingpracticesandachievingsignificantcost/efficiencyleadershipsharedsomecommoncharacteristics:Financialoperationsenterprisereporting,planningandconsolidationswerecompletedinasharedservicestypeenvironment.Mostofthesecompaniessharedacommonchartofaccounts(orwereinthefinalstagesofdefiningacommonchartofaccounts).Bestinclasscompanieshadprogressedintheiruseofe-commerceandenterprisewidetechnologyandalsousedsharedservicescentersastransactionmanagementlocations.Self-Serviceandend-useraccesstoinformationwasarecurringgoalortargetforalmost100%ofthecompaniessurveyed.Theconsolidationanalysthadmovedfromverifyingdataauthenticityandreconciliationtofinancialanalysis.Responsibilityofqualitydataandinformationwaspushedtotheoriginator.Eachoftheenterpriseshadclearprocedures,guidelinesandcontrolsforprocessingdataSTRATEGYORLEADINGPRACTICEGENERALFINDINGS/ILLUSTRATIVEEXAMPLESFinancialReporting1.FinancialinformationisconsistentandaccurateStandardizefinancialreportsacrossLOB’s.Commonchartofaccountsdesignedaroundmanagementreportingwithflexibilityforlocalandstatutoryreportingrequirements.Transactionsarecodedwithsufficientinformationformultiplereportingrequirements.2.StandardizeReportingMinimizead-hocreporting.Ad-hocreporting,whererequired,waspushedtotheend-user,withtheend-userhavingaccesstoreportingtoolsandconsolidateddata.Thetop5companiesutilizedtheinternettoallowend-userad-hocreporting.Utilizestatisticalanalysissoftwarewhenpossible.3.ReportFormatReportshaveaconsistentformatandstyle.Reportsaresimple.Page102/11/99Finance/Accounting–Leading/EmergingPracticesSTRATEGYORLEADINGPRACTICEGENERALFINDINGS/ILLUSTRATIVEEXAMPLESStrictself-imposedreportingguidelinestoachieveconsistencybetweeninternalandexternalreports.4.ReportTimingEliminatereports,whichaddlittlevalue.Eliminatereportsifdeliveryexceedsvalue.Minimizead-hocreporting.Ad-hocreporting,whererequired,waspushedtotheend-user,withtheend-userhavingaccesstoreportingtoolsandconsolidateddata.Thetop5companiesutilizedtheinternettoallowend-userad-hocreporting.Minimizepost-closingtransactions.Synchronizeoperationscalendarsandcut-off’s.Publishareportdistributionschedule;Makestandardreportsavailableonlinetoeliminateconstantrecreation.5.MetricsandMeasuresUsemorethanGLasasourceformanagementinformation.Utilizeabalancedscorecardtomeasureperformance.Reportscontainfinancialandnon-financialmeasurestosupportdecision-makin...