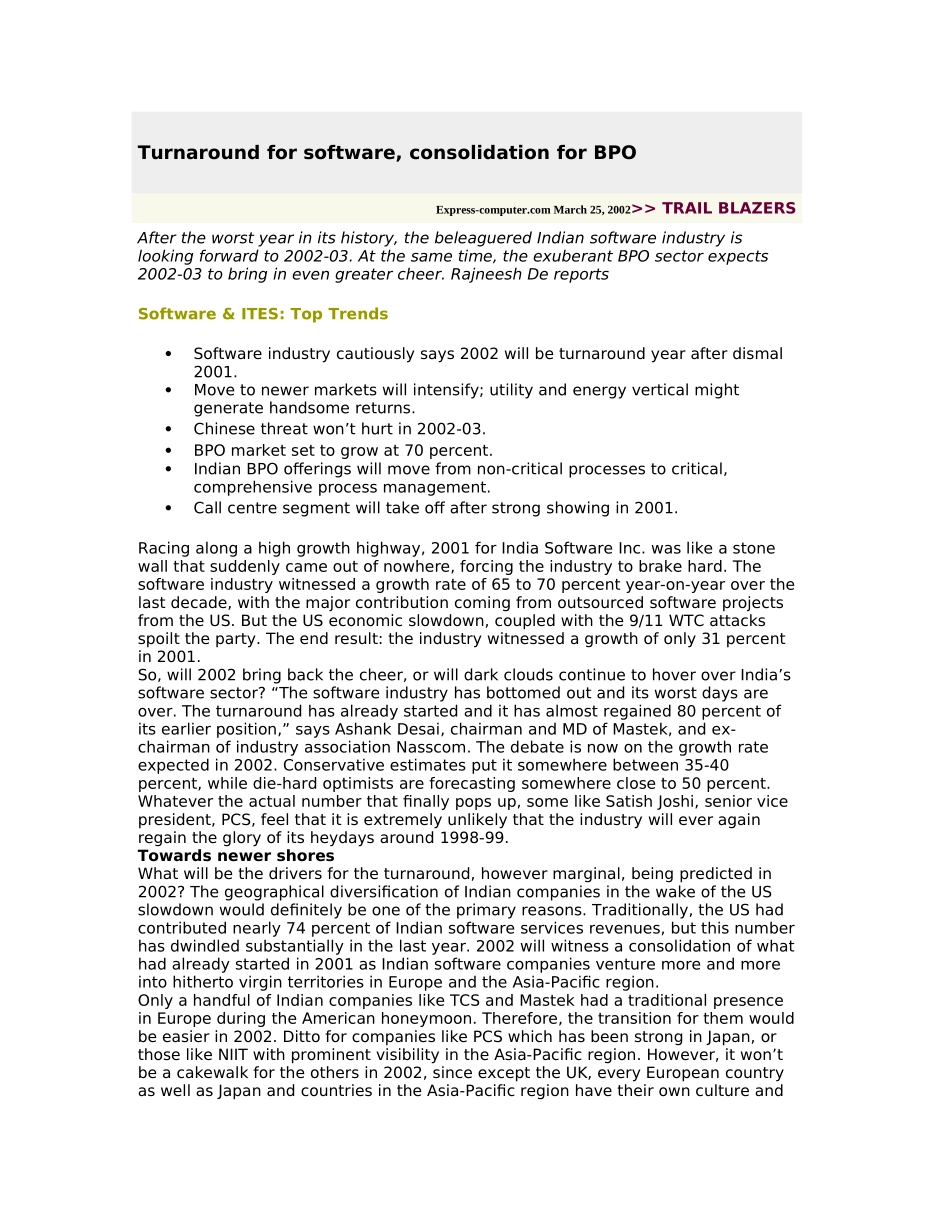

Turnaroundforsoftware,consolidationforBPOExpress-computer.comMarch25,2002>>TRAILBLAZERSAftertheworstyearinitshistory,thebeleagueredIndiansoftwareindustryislookingforwardto2002-03.Atthesametime,theexuberantBPOsectorexpects2002-03tobringinevengreatercheer.RajneeshDereportsSoftware&ITES:TopTrendsSoftwareindustrycautiouslysays2002willbeturnaroundyearafterdismal2001.Movetonewermarketswillintensify;utilityandenergyverticalmightgeneratehandsomereturns.Chinesethreatwon’thurtin2002-03.BPOmarketsettogrowat70percent.IndianBPOofferingswillmovefromnon-criticalprocessestocritical,comprehensiveprocessmanagement.Callcentresegmentwilltakeoffafterstrongshowingin2001.Racingalongahighgrowthhighway,2001forIndiaSoftwareInc.waslikeastonewallthatsuddenlycameoutofnowhere,forcingtheindustrytobrakehard.Thesoftwareindustrywitnessedagrowthrateof65to70percentyear-on-yearoverthelastdecade,withthemajorcontributioncomingfromoutsourcedsoftwareprojectsfromtheUS.ButtheUSeconomicslowdown,coupledwiththe9/11WTCattacksspoilttheparty.Theendresult:theindustrywitnessedagrowthofonly31percentin2001.So,will2002bringbackthecheer,orwilldarkcloudscontinuetohoveroverIndia’ssoftwaresector?“Thesoftwareindustryhasbottomedoutanditsworstdaysareover.Theturnaroundhasalreadystartedandithasalmostregained80percentofitsearlierposition,”saysAshankDesai,chairmanandMDofMastek,andex-chairmanofindustryassociationNasscom.Thedebateisnowonthegrowthrateexpectedin2002.Conservativeestimatesputitsomewherebetween35-40percent,whiledie-hardoptimistsareforecastingsomewherecloseto50percent.Whatevertheactualnumberthatfinallypopsup,somelikeSatishJoshi,seniorvicepresident,PCS,feelthatitisextremelyunlikelythattheindustrywilleveragainregainthegloryofitsheydaysaround1998-99.TowardsnewershoresWhatwillbethedriversfortheturnaround,howevermarginal,beingpredictedin2002?ThegeographicaldiversificationofIndiancompaniesinthewakeoftheUSslowdownwoulddefinitelybeoneoftheprimaryreasons.Traditionally,theUShadcontributednearly74percentofIndiansoftwareservicesrevenues,butthisnumberhasdwindledsubstantiallyinthelastyear.2002willwitnessaconsolidationofwhathadalreadystartedin2001asIndiansoftwarecompaniesventuremoreandmoreintohithertovirginterritoriesinEuropeandtheAsia-Pacificregion.OnlyahandfulofIndiancompanieslikeTCSandMastekhadatraditionalpresenceinEuropeduringtheAmericanhoneymoon.Therefore,thetransitionforthemwouldbeeasierin2002.DittoforcompanieslikePCSwhichhasbeenstronginJapan,orthoselikeNIITwithprominentvisibilityintheAsia-Pacificregion.However,itwon’tbeacakewalkfortheothersin2002,sinceexcepttheUK,everyEuropeancountryaswellasJapanandcountriesintheAsia-Pacificregionhavetheirowncultureandbusinessprocesses,whichrequiresometimeandefforttoadaptto.Geography-wise,thelikelyrevenuespreadin2002wouldbearound55to60percentfromtheUS,30to35percentfromEuropeandanother10percentfromJapan.VerticalsandservicelinesFinancialservicesandinsurancearetwoverticalswhereIndiancompanieshavetraditionallybeenstrongin,andthistrendislikelytocontinuein2002.Manufacturingandretailarealsogoingtobeverticalswithsubstantialrevenuepotential.However,thecommonbeliefisthattheutilityandenergyverticalmightturnouttobethedarkhorse,especiallyafterthederegulationoftheUSenergysector.However,thehospitalitysector,anothersignificantrevenueearner,wasbadlyhitpost-9/11,andislikelytoremaininthedoldrumsthisye...