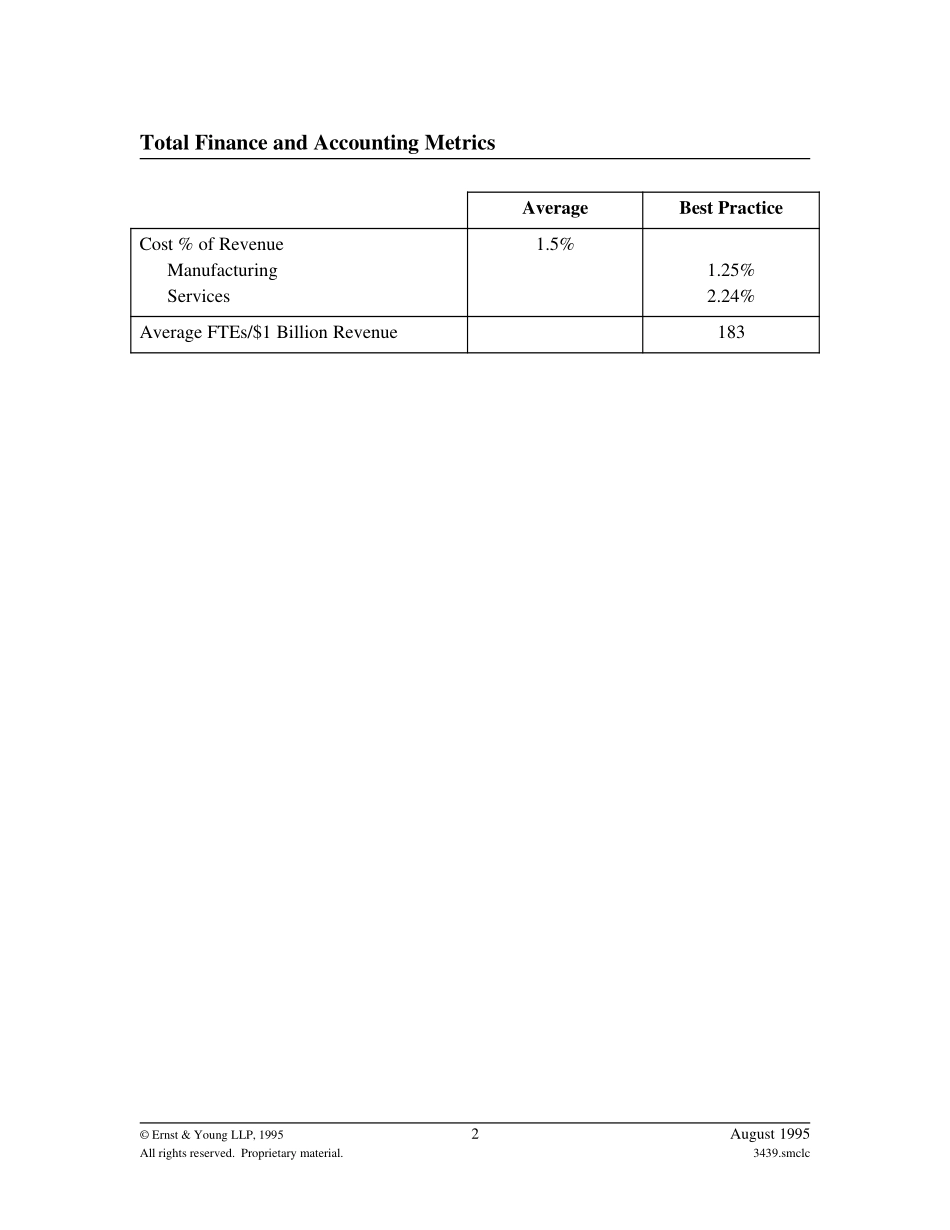

IntroductionToday,Ernst&Youngiscontinuouslychallengedtounderstandourcustomer’severchangingbusinessneedsandrequirements.Recognizing,understanding,andsuccessfullyaddressingtheseneedsisvitaltotheongoingsuccessofourcustomersandErnst&Young.OurcustomersarechallengingErnst&Youngtounderstandandaddressanareaoftheircompanythattheyhavenottraditionallyfocusedon-financialprocessdesign.Ourcustomersrecognizethatfocusingonfinancialsystemenhancementsorcompletereplacementwillnotallowthemtoachievetheiroptimumgoals.Theirentirefinancialprocessmustimprove.Aprocessisdefinedasasetofinterrelatedactivitiesorfunctionsthattogether,achieveaspecificgoal.Therefore,systemenhancementsorreplacementsalonewillnotsuffice.Newpoliciesandproceduresmustbeestablishedandawillingnesstochangemustbeadaptedbythecustomersinorderforthenewprocesstosucceed.ThischangeinprocessdesignisreferredtoasFinancialProcessReengineering.TheFinanceandAccountingBestPracticesandBenchmarksinthisdocumentrepresentleadingedgecharacteristicsofcorporations.ThisdocumentisutilizedasahighleveloverviewofBestinClassdata.Thecontentsofthisdocumentareconfidentialandintendedforusebythebenchmarkingparticipantsonly.NoreproductionofthisdocumentisallowedwithouttheconsentofErnst&Young.©Ernst&YoungLLP,19951August1995Allrightsreserved.Proprietarymaterial.3439.smclcTotalFinanceandAccountingMetricsAverageBestPracticeCost%ofRevenueManufacturingServices1.5%1.25%2.24%AverageFTEs/$1BillionRevenue183©Ernst&YoungLLP,19952August1995Allrightsreserved.Proprietarymaterial.3439.smclcAccountsPayableBestPracticeCharacteristics1.OnesharedservicesAccountsPayabledepartment.2.Integratedfinancialsystem,allinformationavailableelectronically.3.Informationcaptured(entered)atsource.4.POdriven,field-generatedforroutinepurchases.5.MaximizePO-drivenpurchases.6.Oneprocessusedforallpurchases.7.On-lineverificationandapprovalofPOinformation.8.On-lineinquiry.9.Payableuponreceipt(2-waymatch)whenpossible.(EvaluateReceiptSettlement)10.EDIwithsuppliers.11.Maintainon-lineprocurementcatalog.12.APinvolvedincontractnegotiations-paymentsmethods.13.Opticalimagingofhighretrievalratedocuments.14.Controlfocusonmaterialexpectationsandsampling.15.Purchasingagentusedonlyforcomplexpurchases.16.Minimalnumberofvendors.17.Contracttermsdefinepaymenttermsandpaymentmethod.18.Policiesunderconstantreview.19.AutomaticpostingtoGL.©Ernst&YoungLLP,19953August1995Allrightsreserved.Proprietarymaterial.3439.smclcPaymentMetricsAverageBestPracticeAPFTEper$1BillionRevenue208-12DaystoProcessandInvoice<4<2APLaborCost/VendorInvoice$3.00$1.00APLaborCost/Revenue0.09%<.05%AnnualVendorInvoices/APFTE13,000>20,000WagesandBenefits/APFTE$36,000AgeofAPSystem5.5yearsAPSpanofControl1:9.7PercentageofPaymentsmadeFTE>80%PercentageofERSVendors>75%PercentageofPayablesPODriven>95%InvoiceReviewPercentageRequiredtoAnalyze80%1%FreightPaymentFTE/$1BillionRevenue21FreightPaymentLaborCost/Revenue0.02%.001%FreightPaymentInvoices/FreightPaymentFTE20,00044,500FreightPaymentLaborCost/FreightPayments$2.00$.65©Ernst&YoungLLP,19954August1995Allrightsreserved.Proprietarymaterial.3439.smclcEmployeeExpenseReportsBestPracticeCharacteristics1.Employeepayablesarepaidwithpayrollfromasinglesystem.2.Integratedfinancialsystem,allinformationavailableelectronically.3.Informationcapturedatsource.4.On-lineverificationandapproval.5.On-lineinquiry.6.Archives-on-line...