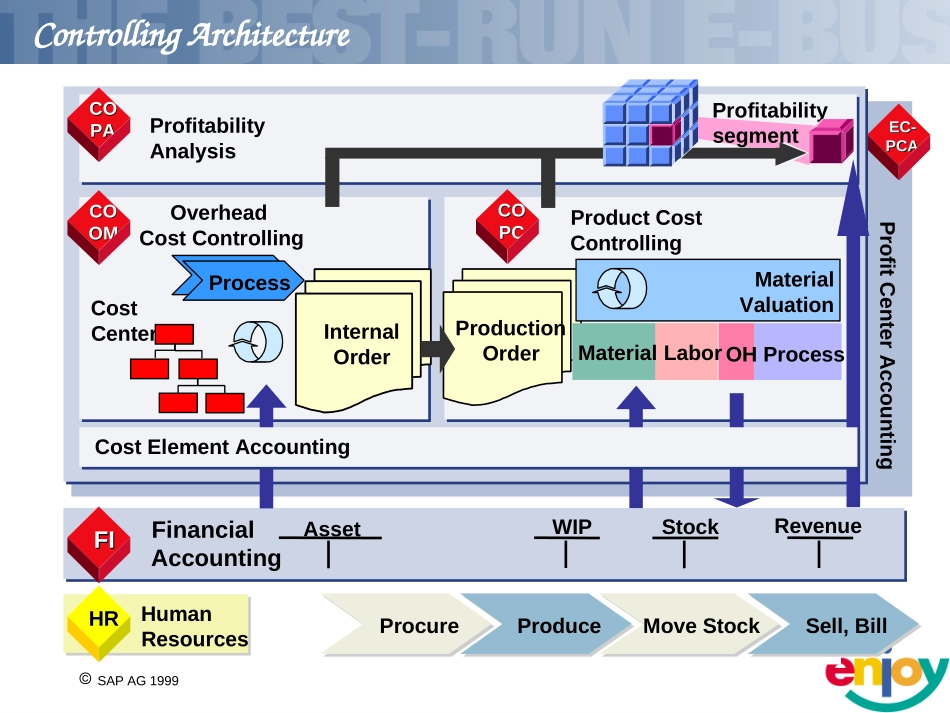

SAPAG2001,SolutionDeliverManager,CharterLuo1OverheadCostControllingOverheadCostControllingJACOBWANG王呈晃2005/09/28OverheadAccountingOverviewExpenseAllocationSplittingActualPriceCalculationRevaluationAGENDAControllingArchitectureSAPAG1999EC-EC-PCAPCAHRHRCOCOPCPCProductionOrderProcessInternalOrderMaterialValuationCostCenterProfitCenterAccountingProductCostControllingOverheadCostControllingHumanResourcesCOCOOMOMCOCOPAPAProfitabilitysegmentFinancialAccountingFinancialAccountingAssetWIPRevenueFIFIStockMaterialLaborOHProcessCostElementAccountingCostElementAccountingProcureProduceMoveStockSell,BillProfitabilityAnalysisOverheadAccountingOverviewExpenseAllocationDistributionAssessmentRepostingSplittingActualPriceCalculationRevaluationExpenseAllocationExpensePosting420000DirectLabor416100Overhead612000DepreciationExpenseServiceCostCenter420000600041610010006120002000Total9000FIMMAMExpenseDistributionServiceCostCenter420000600041610010006120002000Total9000DirectCostCenter42000030004161005006120001500Total9000DirectCostCenter4200003000416100500612000500Total9000Distribution(KSV1-KSV5)30%20%50%1000-Service1000-Service416100+6,900416110+1,500416100+4,600416110+1,000416100+11,500416110+2,500Tracingrule:Forexample,fixedpercentagesElectricityJanuaryEnergycostcenter416100+23,000416110+5,000416100-23,000416110-5,000Energycostcenter416100+23,000416110+5,000416100-23,000416110-5,0003200-Marketing3200-Marketing1220-Vehicles1220-VehiclesAssessment(KSU1-KSU5)420000DirectLaborcostsinJanuary416100Electricity612000PlantmaintenanceCafeteria420000600041610010006120002000Total9000631000631000-9000-9000Assessment(cafeteria)Tracingrule:Forexample,statisticalkeyfigures(Employees)Employees30Employees10Employees501000-Service1000-Service1220-Vehicles1220-Vehicles3200-Marketing3200-Marketing631000+3000631000+1000631000+5000Reposting(KSW1-KSW5)1000200020001000-Service1000-Service416100+4,600416110+1,000416100+9,200416110+2,000416100+9,200416110+2,000Tracingrule:Forexample,fixedPotionElectricityJanuaryEnergycostcenter416100+23,000416110+5,000416100-23,000416110-5,000Energycostcenter416100+23,000416110+5,000416100-23,000416110-5,0003200-Marketing3200-Marketing1220-Vehicles1220-VehiclesCycleCreation–CreateCycleName(KSV1/KSU1/KSW1)Allocation/Assessment/Reposting的Cycle名稱不能重複CycleCreation–DefineHeaderDataCycleCreation–DefineSegmentHeaderCycleCreation–DefineSender/ReceiverCycleCreation–SenderValuesCycleCreation–DefineReceiverTracingFactorCycleCreation–ReceiverWeightFactorsExecuteCycle(KSV5/KSU5/KSW5)ResultofCycleResultofDistribution-SenderResultofDistribution-ReceiverResultofAssessment-SenderResultofAssessment-ReceiverResultofReposting-SenderResultofReposting-ReceiverOverheadAccountingOverviewExpenseAllocationSplittingActualPriceCalculationRevaluationSplittingDirectCostCenter42000030004161005006120001500Total9000LaborActivityType4200003000Machine1ActivityType6120001000Machine2ActivityType612000500OverheadActivityType416100500ExecuteSplitting(KSS2)ResultofSplittingOverheadAccountingOverviewExpenseDistributionSplittingActualPriceCalculationRevaluationActualPriceCalculationLaborActivityType4200003000(A)1000(Q)3(P)Machine1ActivityType4200001000(A)2000(Q)0.5(P)Machine2ActivityType420000500(A)2000(Q)0.4(P)OverheadActivityType420000500(A)500(Q)1(P)ActualPriceActualPriceActualPriceActualPriceExecuteActualPriceCalculation(KSII)ResultofActualPriceCalculationDisplaytheActualPrice(KBK6)OverheadAccountingOverviewExpenseAllocationSplittingActualPriceCalculationRevaluationRevaluationLaborActivityType4200003000(A)1000(Q)3(AP)ActualPriceOrder1Order2Order32.5(PP)PlanPrice7100000000125071000000007507100000000500710000000025071000000001507100000000100ExecuteRevaluation(CON2)ResultofRevaluationAdjustmentinOrderTeatimeQ&A