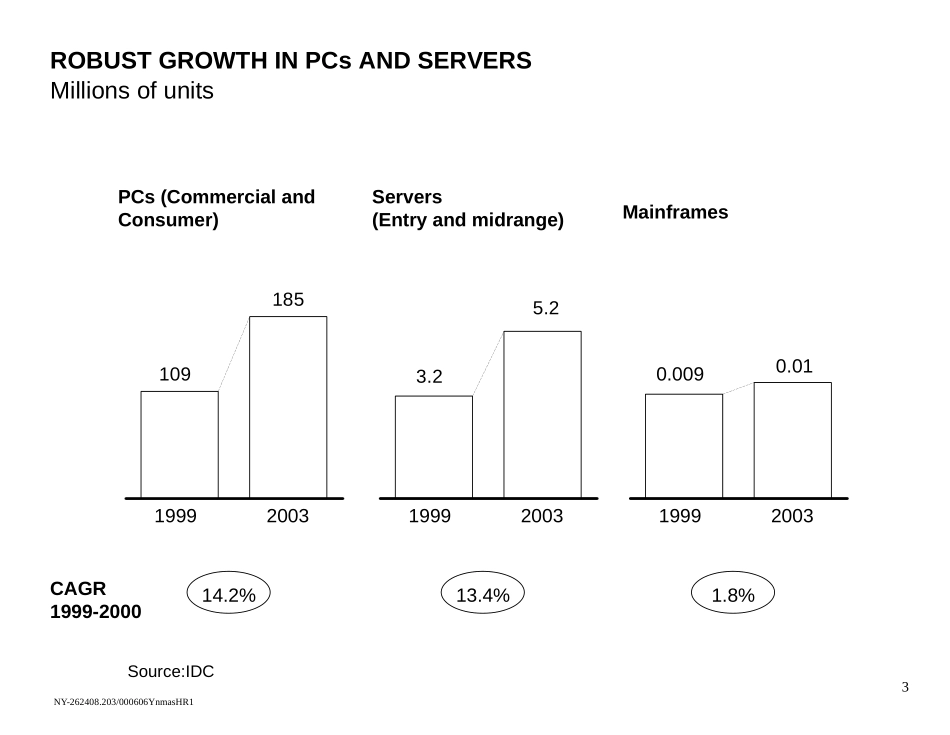

NY-262408.203/000606YnmasHR1CONFIDENTIALDiscussionDocumentJune14,2000ComputerIndustryDynamicsHIGHTECHCOREGROUPTRAININGPROGRAMNY-262408.203/000606YnmasHR12Thecomputerindustryiscontinuingtogrowrobustly.Thegrowthisbeingacceleratedbynewsegmentswhicharechangingtheoveralllandscapeandcompetitivedynamics.Increasinglymanyplayersarelookingtootherelementsinthevaluechaintogainprofitsandnewstandardsbattlesareemerging•PCplayershaveexperiencedfundamentalchangeasdirectplayersgainedground.Furthermoredirectplayersareleadingthechargetocaptureprofits“beyondthebox”andtoexploitnon-Wintelinformationappliances.Indirectplayerswillcontinuetohaveadifficultgameofcatch-up•Servergrowthhasbeendrivenbytheinternet.Theemergenceof“applicationservers”maybethetriggerforalongrumoredgrowthofLinux•Storagesystemshaveemergedasasizableandhighlyprofitablesegment,andarenotsimplyperipheralstoservers.Theemergenceofnewstoragearchitectures,particularlystorageareanetworks(SAN),createadiscontinuitythatwilllikelyimpactstorageandrelatedcomputersegmentsfromserverstosoftware.•Smarthandheldsareemergingasthenextgrowthengine.AdiversesetofdevicesareemergingthatcouldfundamentallythreatentheWintelmonopoly.ButnewOSstandardsownersarenotlikelytocaptureMicrosoftlikeprofitsasasignificantshareofthevalueisexpectedtomigratefromhardwaretoservicesCOMPUTERINDUSTRYDYNAMICSNY-262408.203/000606YnmasHR1318510919992003ROBUSTGROWTHINPCsANDSERVERSMillionsofunitsPCs(CommercialandConsumer)14.2%CAGR1999-20005.23.219992003Servers(Entryandmidrange)13.4%19992003Mainframes1.8%0.0090.01Source:IDCNY-262408.203/000606YnmasHR14BUTAVERAGESELLINGPRICESAREFALLINGPCsDollars-6.2%AveragepricedeclineServers*$Thousands-3.6%Mainframeservers$Millions-4.4%1,0001,2001,4001,6001,8002,00019992003101214161820199920031.01.21.41.61.82.019992003*EntryandmidrangeSource:IDCKeyfactorscausingASPdecline•Increasedpricedeclineduetocommoditization•Industryshifttowardsmorecost-effectivedirectdistributionmodels•Industryshifttowardsmoreefficientmanufacturing,e.g.,one-touchprocessNY-262408.203/000606YnmasHR151702238968ServersPCs19992003238312REVENUEGROWTHLACKLUSTEREXCEPTINNEWSEGMENTSRevenue$BillionsComputerSystems7.0%6.9%7.0%CAGR1999-20031702236889641763218OtherApplianceserversPCs19992003277401ComputerSystemsplusnewsegments7.0%6.9%18.6%CAGR1999-2003StoragesystemsServersSmarthandhelds28.0%83.4%9.7%Source:IDCNY-262408.203/000606YnmasHR16Thecomputerindustryiscontinuingtogrowrobustly.Thegrowthisbeingacceleratedbynewsegmentswhicharechangingtheoveralllandscapeandcompetitivedynamics.Increasinglymanyplayersarelookingtootherelementsinthevaluechaintogainprofitsandnewstandardsbattlesareemerging•PCplayershaveexperiencedfundamentalchangeasdirectplayersgainedground.Furthermoredirectplayersareleadingthechargetocaptureprofits“beyondthebox”andtoexploitnon-Wintelinformationappliances.Indirectplayerswillcontinuetohaveadifficultgameofcatch-up–WhiteBoxmarketrepresentsasizeablesharebecauseofcommoditization,pressuringmargins–PCcompaniesarelookingtootherrevenuesourcesforprofits.–Thedirectplayershavetakenmarketsharefromindirectplayers–Delliscontinuingtoout-executecompetitorswithsuperiorcustomerinteractionandoperationalmodels–Indirectmodelwillnotdisappear,butplayersneedtoincreasecompetitiveness•Servergrowthhasbeendrivenbytheinternet.Theemergenceof“applicationservers”maybethetriggerforalongru...