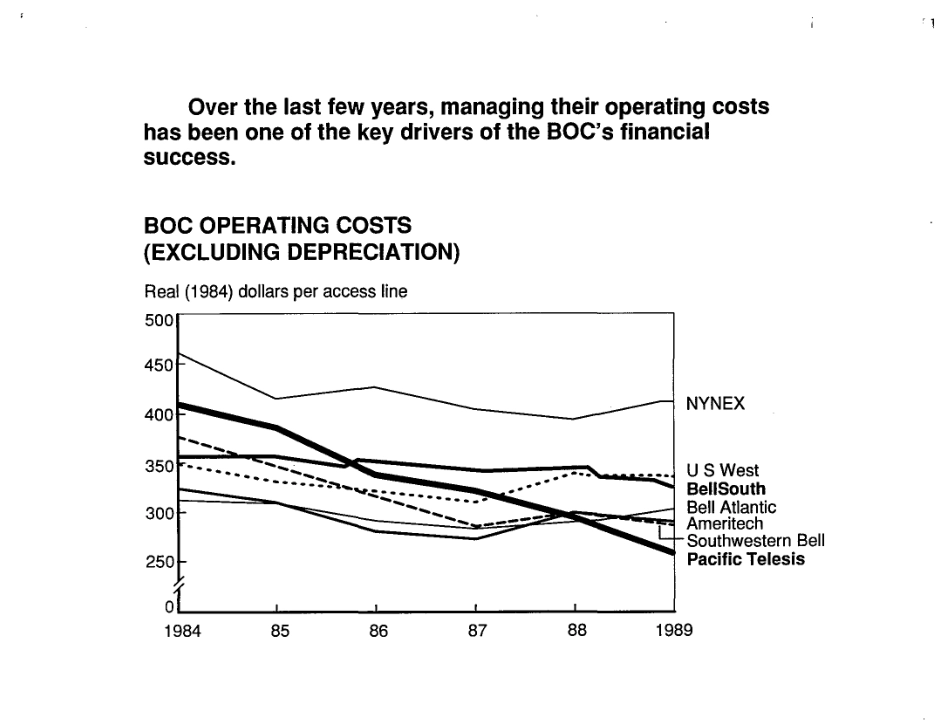

BETTEGER~D–CHACHIEVINGPROFITIMPROVEMENTSATTELECOMSERWCEPROVIDERS1992WORLDWH)ETELECO~ICATIONSCONFERENCE,CHICAGO,ILLINOIS,FEBRUARY13–141992Date:U92Sech~TELECOMMUNICATIONSKeywordsPROFITIMPROVEMENT/COSTREDUCTIONUse:INTERNALONLYManagingoperatingcostshasbeenoneofthekeydriversoftheBellOperatingCompanies(BOC)financialsuccess.In1991mostoftberegionalholdingcompanies(RHC)down-sizedtoremaincompetitive.However,competitivepressureswillcontinuetogrow.McKinseymustleverageexperienceinprofitimprovementworkfromotherindustries,andtailorthoseapproaches,toproactivelyfulfilltherealoppotiitiesinquantuInleapimprovementprograms.ACHIEVINGPROFITIMPROVEMENTSATTELECOMSERVICEPROVIDERS1992WorldwideTelecommunicationPracticeConferenceFebruary13,1992IOverthelastfewyears,managingtheiroperatingcostshasbeenoneofthekeydriversoftheBOC’Sfinancialsuccess.BOCOPERATINGCOSTS(EXCLUDINGDEPRECIATION)Real(1984)dollarsperaccessline‘oo~‘YNEX350---—300-—----*USWestBellSouth---BellAtlanticAmeritech}-SouthwesternBell250PacificTelesis41984858687881989In1991,mostoftheRHCSexperiencedTOTALRETURNSTOSHAREHOLDERS*PercentCAGR1984-8617.51–2.414.187-891990-3/91anewsensation.ROECOMPARISON19901991AmeritechBellAtlanticBellSouthNYNEXPacTel6.314.54.8–2.9**2.811.30.26.43.713.2Southwestern12.912.3BellUSWest13.75.7“Includesreinvestmentofdividends“’Reflectsaccountingwrhe-offforhealthcare.7Manyofthemrevertedbacktotheproventoolsofearlyretirementprograms.ExpectedCompanyheadcountreductionCommentsAmeritech2,100-19912,300-1992-96BellAtlantic3,500-1991AllBellAtlanticreductionshavebeenvoluntarytodateBellSouth4,250-19913,000-1992NYNEX1,000–1990’Mostofthefuturereductionswillcomefrom.Iayoffs1,900-19921,500–1993-94PacTel4,300-1991PacTelwanted3,000volunteers,got4,30011,000–1992-941992-94cutsrepresent19V0oftotalmanagersand17V0ofnonmanagersSouthwesternBell1,100-1990SouthwesternBellwentfromvoluntarystaffreductionsin3,750–19911990and1991toforcedreductionsin1992300–1992USWest3,850–1990Managersonly6,000–1992-?Managersandnonmanagers50,000.approximatesizeofPacTel“EstimetedHowever,competitivepressureswillcontinuetogrow.EXAMPLE:THREATFROMALTERNATIVEACCESSVENDORS:BASICAAVMARKETGROWTHSTATISTICSNumberAAVNetworkofcitiesrouteinvestmentwithAAVSmiles$Millions1987513319889188$24198913724501990251,156100199140+250GrowthdriversEnd-userperspective“Technicalqualityofservice“Responsivenesstocustomerneeds(e.g.,provisioningandrepairintervals).PriceIXCperspective“Costreduction(accessequals40-50%oflongdistancerevenues)-Sameasend-userperspective%urce:FCC;EasternManagementGrorJp;YankeeGroupOverall,theenvironmentcontinuestoundergodramaticchanges..Alternativeaccessvendorspushingforinterconnection,switchedaccess,andco-location.Intra-latatollmonopoliesarebeingopenedup.Alternativeoperatorservicesemerge.Newmobiletechnologiesthreatenthewireloop.RegulatorsarethreateningtolowerallowedROEGInformationservicesmarketopenedasthenext“big”opportunityInlightofalltheseevents,telcosarefacedwithamoredramaticchallengethanjusttoreducetheirheadcount.KEYCHALLENGESGGGGGGGenerategrotihinthecorebusinessRadicallyrestructurecostbaseImprovecustomerserviceDeploynextgenerationtechnologiesFocusorganizationexternallyonmarketperformanceNegotiatewithregulatorstocaPturevGPromotecorebusinessperformanceimprovementsRestructureandfocusorganizationalcapabilitiesChallengeestablishedwisdomthe-’’fruits”ofrest~ucturing“Matchingthissituationwithourpastpracticemixsuggeststhatwemaynotbewellpreparedtoaddresstheissuesfacedbyourclientsintheircorebusinessessinceinthepaststrategyworkhasbeenthedominantpartofthepractice...STRATEGYASPERCENTOFSTUDIESBYREGION-WORLDWIDEThousandsofhours;percent98.3AmericasEuropeUnitedStatesPacificBasinWorldwideCUMULATIVE100%=296,000WorldwideoAmericas579%PacificBasin17%~oYOUnitedStates1g~oEurope19878889901991...andoperationsworkhasinfactdeclinedoverthelastcoupleofyears.OPERATIONSASPERCENTOFSTUDIESBYREGION-WORLDWIDEThousandsofhours;percent76.2n\IIIi,///I“\\\\\\58.2;;;/’\T,\\\;;I\\‘\\\39.1!’;/\\y:\38.1//\I1,\\‘4~o—Americas1’11’\39Europe/if\\/’16.4;;,It/I\r/11\\54UnitedStatesIf\‘.\‘\OPacificBasin419878889<3Worldwide901991CUMULATIVE100%=228.21.7%=’3.9AmericasEuropeUnitedStatesThissituationsetsthestageforamorecomprehensiveMcKinseyresponse.McKINSEYPOSSIBLERESPONSE.LeverageoutstandingexperienceinprofitimprovementworkfromotherindustriesGUnderstandtheuniquetelcoenvironment.Tailorapproaches.ProactivelyfulfilltherealopportunitiesinquantumleapimprovementprogramsTheremainderofthisafternoonwillcoverseveraltopics.TopicsCommentsDeltaPBuildingInstitutionalSkillsChangeManagementCustomerSatisfactionCoreProcessRedesignISSupportofProductIntroductionImprovingPerformanceofTelcosThroughIT1“Richpractice,TelecomAustraliawasatestbedexperience.ComprehensiveculturechangeprogramsCanbeusedasanenergizingthemefortheentireorganizationtochangebehaviorRevisitstheexistingparadigms,growingexperiencebase1Opportunitiestoleveragenewskillsetincombinationwithotherexperiences