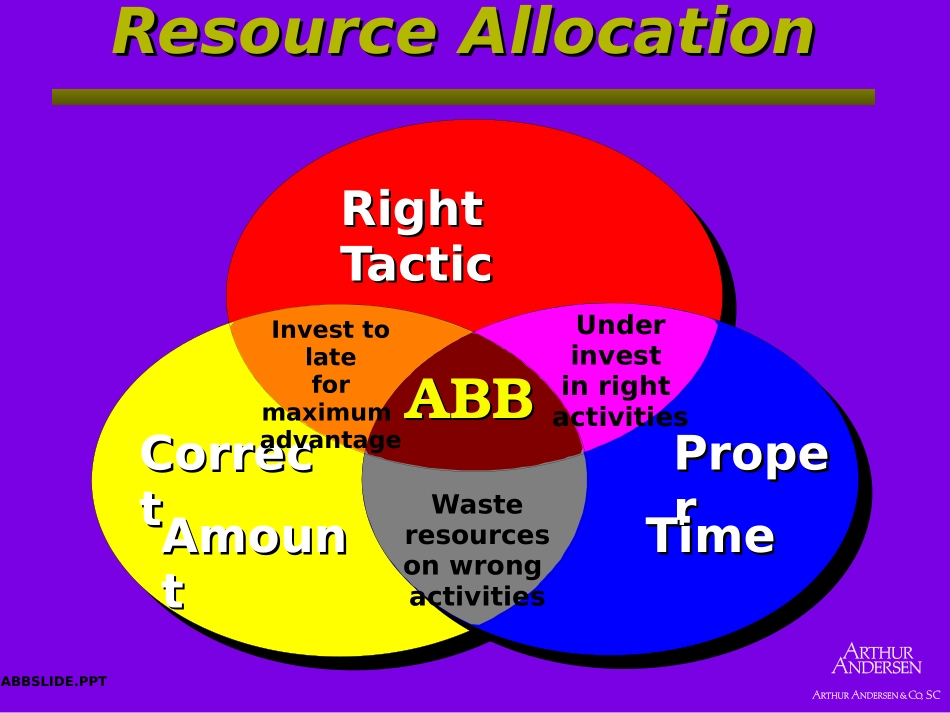

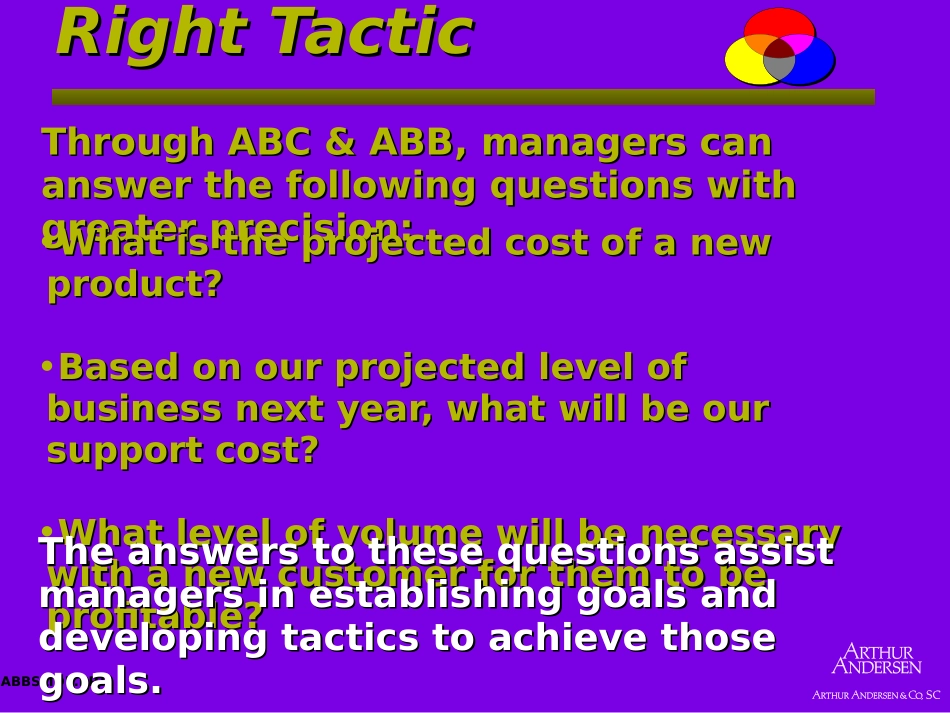

ABBSLIDE.PPTIntroductiontoIntroductiontoActivityBasedActivityBasedBudgetingBudgetingConceptsConceptsABBSLIDE.PPTResourceAllocationResourceAllocationRightRightTacticTacticPropeProperrCorrecCorrecttUnderinvestinrightactivitiesWasteresourcesonwrongactivitiesInvesttolateformaximumadvantageAmounAmounttTimeTimeABBABBABBSLIDE.PPTRightTacticRightTacticThroughABC&ABB,managerscanThroughABC&ABB,managerscananswerthefollowingquestionswithanswerthefollowingquestionswithgreaterprecision:greaterprecision:•WhatistheprojectedcostofanewWhatistheprojectedcostofanewproduct?product?•BasedonourprojectedlevelofBasedonourprojectedlevelofbusinessnextyear,whatwillbeourbusinessnextyear,whatwillbeoursupportcost?supportcost?•WhatlevelofvolumewillbenecessaryWhatlevelofvolumewillbenecessarywithanewcustomerforthemtobewithanewcustomerforthemtobeprofitable?profitable?TheanswerstothesequestionsassistTheanswerstothesequestionsassistmanagersinestablishinggoalsandmanagersinestablishinggoalsanddevelopingtacticstoachievethosedevelopingtacticstoachievethosegoals.goals.ABBSLIDE.PPTProperTimeProperTimeThroughABBmangerscananalizeThroughABBmangerscananalizecapacityplanningthroughexaminingcapacityplanningthroughexaminingthebehaiourofcostthroughthethebehaiourofcostthroughtheplanninghorizon.planninghorizon.ActualActualCostCostBudgetedBudgetedFixedActivityFixedActivityBudgetedFixedBudgetedFixedActivityUsageActivityUsageBudgetBudgetVarianceVarianceCapacityCapacityVarianceVariance110hrs=110hrs=$5,000$5,000100hrs=100hrs=$6,000$6,00090hrs=90hrs=$5,400$5,400$600$600UU$1,000$1,000FFFixedCostFixedCostAnalysisAnalysisABBSLIDE.PPTCorrectAmountCorrectAmountThroughthepowerofABC,mangerscanThroughthepowerofABC,mangerscanunderstandthe“true”costassociatedunderstandthe“true”costassociatedwithproducts,customersanddivisions.withproducts,customersanddivisions.ABBleveragesthispowerby:ABBleveragesthispowerby:•BeingabletoestimatethefuturecostBeingabletoestimatethefuturecostassociatedwithagivenlevelofactivityassociatedwithagivenlevelofactivitybasedonaforecastedcoststructureofbasedonaforecastedcoststructureofthecompany.thecompany.•BeingabletobetterassessthefinancialBeingabletobetterassessthefinancialimpactofnewmarketing,re-impactofnewmarketing,re-engineering,oroutsourcinginitiativesengineering,oroutsourcinginitiativesbyrelatingthemtolevelsofactivitiesinbyrelatingthemtolevelsofactivitiesinthebusiness.thebusiness.ABBSLIDE.PPTVolumeofActivityResourceDriversEmployeeTime%EmployeeTime%ActualUsageEquipmentUsageLaborFringesSuppliesDepreciationResources$$$$ResourceCostAActivitctivityyBBudgetinudgetinggBBaseaseddABBSLIDE.PPTResourceCostLaborFringesSuppliesDepreciationABCModelProjectedActivityCostProjectedActivityVolumeBudget*=$$$$AActivitctivityyBBudgetinudgetinggBBaseaseddABBSLIDE.PPT$20$50ActivityVolumeCostPerUnitofActivityActivity1Activity2150200________$3,000$10,000LaborFringeSuppliesDepreciation$800$200$50$250____$13,000GeneralLedgerBudgetActivityBasedBudget=AActivitctivityyBBudgetinudgetinggBBaseasedd+