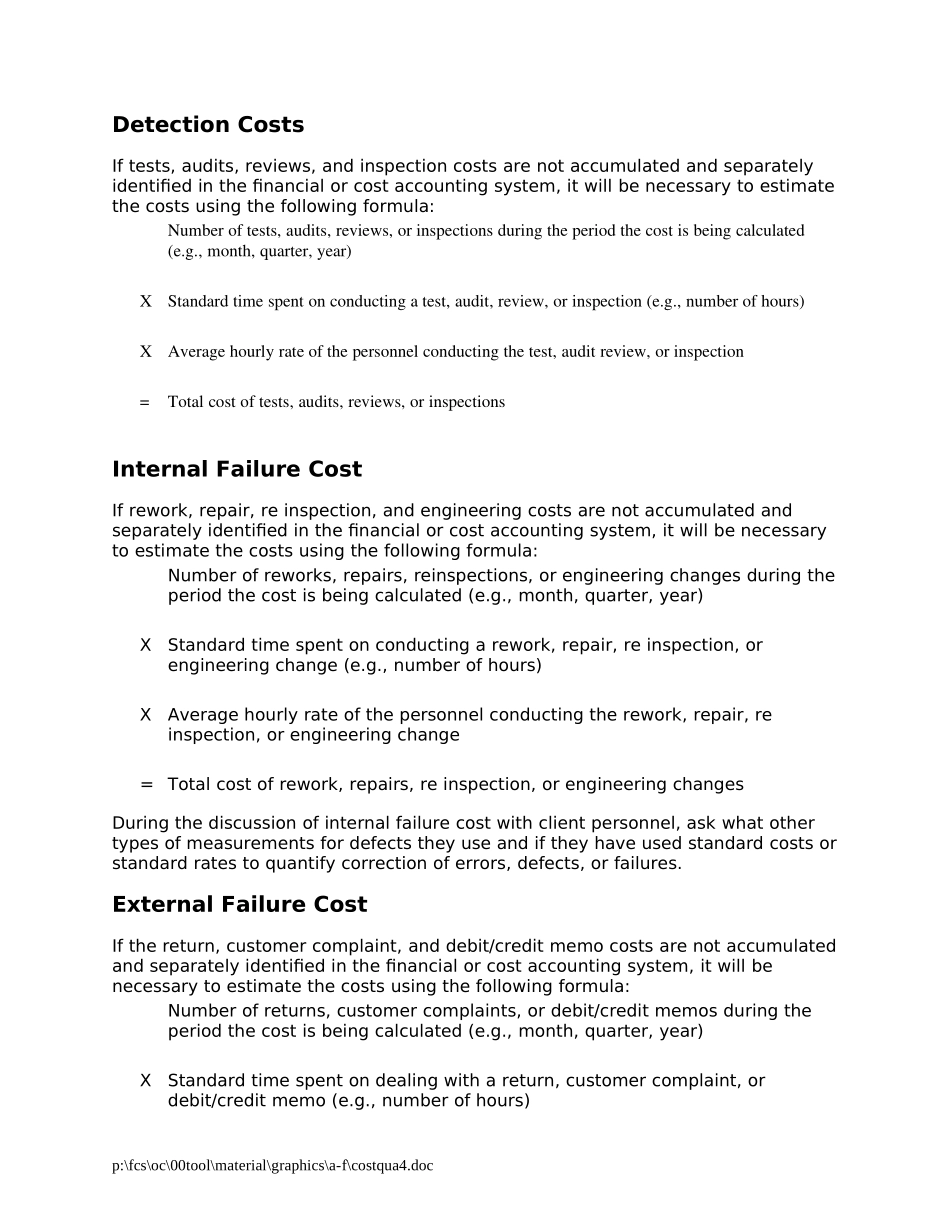

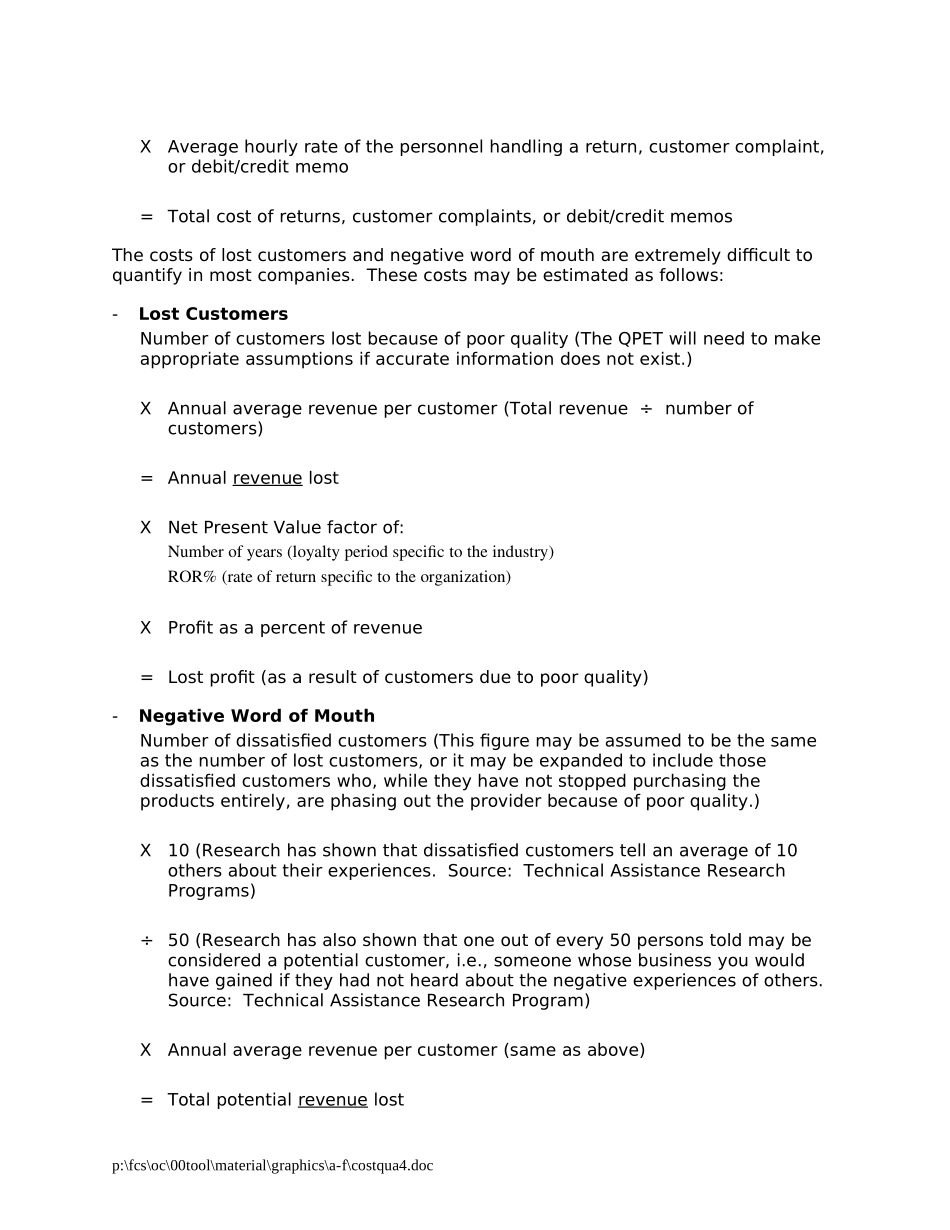

TheCoqCalculationTheCOQcalculationisaguidelinefortheengagementteamtouseindesigningaspecificCOQformulaforthecompanybeingevaluated.ItisimportantfortheclienttohaveaCOQcalculationtailoredtothecompany'squalityprocess,accounting,costaccounting,andothersystemstoenableittodothefollowing:-ContinuecalculatingCOQ.-TakeactiontoreduceCOQ.-Placetheappropriateamountofemphasisonprevention,detectionandfailurecosts.ManycompanieswillbecalculatingCOQforthefirsttime.Therefore,thiswillbethebaseCOQtheywillusetocompareCOQcalculatedinthefuture.ItwillbecomeapowerfultoolforthesecompaniesastheycontinuetousetheformuladesignedtocalculateCOQandtracktheimprovementinthemixofCOQandtotalCOQ.TheCOQmaybeasignificantamountandistypically15to25percentofrevenues,orhigher.Theamountitselfisnotasimportantashowmanagementusestheinformation.TheCOQincludessomehardfacts,straightfromtheaccountinginformation.Italsoincludesestimatedcoststhattypicallyarenotquantified(e.g.,badwill,norepeatcustomers,etc.).However,itisimportanttoincludeanestimatefortheseintangiblecosts.Ifyoudon'tmeasureit,youcan'tcontrolit.EmphasisshouldbeplacedondesigningasoundCOQcalculationframeworkthattheclientcanapplyregularlytoobtainaconsistentCOQ.Accuracyisimportant,butconsistencymakesCOQanevenmorepowerfultooltobeusedforcontinuousqualityimprovement.ThebaseCOQcalculationisquitesimple:P+D+I+E=TCOQTCOQ÷TotalRevenue=TCOQasaPercentofRevenueP=PreventionCostsD=DetectionCostsI=InternalFailureCostsE=ExternalFailureCostsTCOQ=TotalCostofQualityAsthecostelementsarereviewed,theengagementteamandtheclientshoulddeterminewhatpercentageofeachcostelementisquality-related(e.g.,employeeorientation-75percentisnonquality-relatedcompanyoperationsand25percentisintroductiontothequalityprogramandprocedures).Theassumptions,support,andconclusionsshouldbedocumentedtohelpbuildconsensusonthecostelements.p:\fcs\oc\00tool\material\graphics\a-f\costqua4.docDetectionCostsIftests,audits,reviews,andinspectioncostsarenotaccumulatedandseparatelyidentifiedinthefinancialorcostaccountingsystem,itwillbenecessarytoestimatethecostsusingthefollowingformula:Numberoftests,audits,reviews,orinspectionsduringtheperiodthecostisbeingcalculated(e.g.,month,quarter,year)XStandardtimespentonconductingatest,audit,review,orinspection(e.g.,numberofhours)XAveragehourlyrateofthepersonnelconductingthetest,auditreview,orinspection=Totalcostoftests,audits,reviews,orinspectionsInternalFailureCostIfrework,repair,reinspection,andengineeringcostsarenotaccumulatedandseparatelyidentifiedinthefinancialorcostaccountingsystem,itwillbenecessarytoestimatethecostsusingthefollowingformula:Numberofreworks,repairs,reinspections,orengineeringchangesduringtheperiodthecostisbeingcalculated(e.g.,month,quarter,year)XStandardtimespentonconductingarework,repair,reinspection,orengineeringchange(e.g.,numberofhours)XAveragehourlyrateofthepersonnelconductingtherework,repair,reinspection,orengineeringchange=Totalcostofrework,repairs,reinspection,orengineeringchangesDuringthediscussionofinternalfailurecostwithclientpersonnel,askwhatothertypesofmeasurementsfordefectstheyuseandiftheyhaveusedstandardcostsorstandardratestoquantifycorrectionoferrors,defects,orfailures.ExternalFailureCostIfthereturn,customercomplaint,anddebit/creditmemocostsarenotaccumulatedandseparatelyidentifiedinthefinancialorcostaccountingsystem,itwillbenecessarytoestimatethecos...