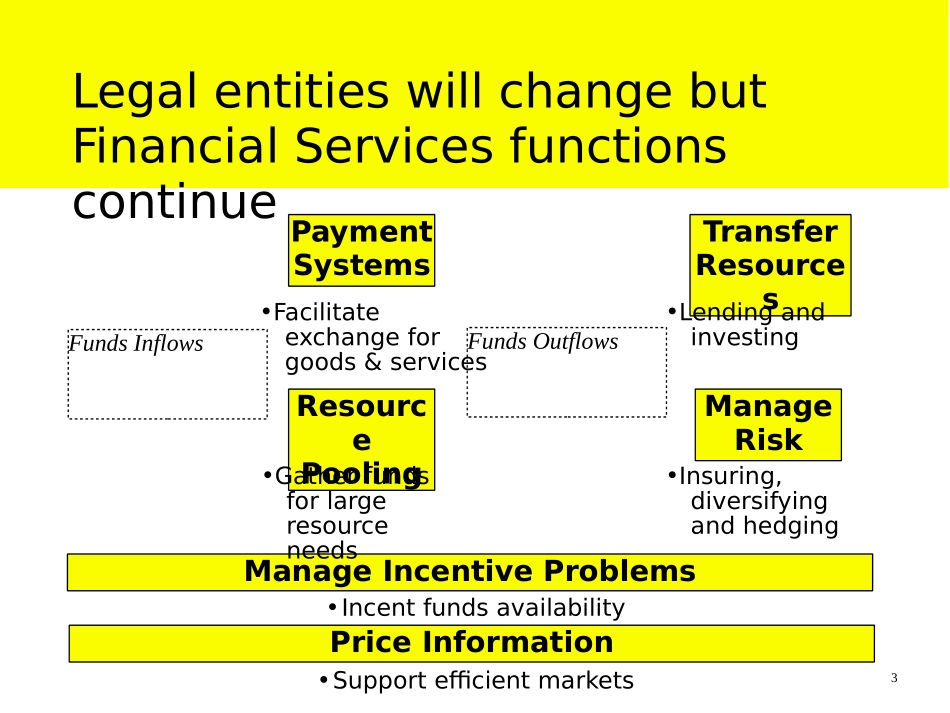

BuildingGlobalIndustryTeamsBusinessConsultingWorldwideWorkshopFinancialMarketsIndustrySessionDecember12,19962FinancialServicesConsultingOffersSignificantOpportunities•FinancialServiceswillgeneratesustainedconsultingneed•Wehaveopportunitiesto•Leverageourexistingskills•Redefineourrole•CreateaglobalFinancialServicesvalueproposition3LegalentitieswillchangebutFinancialServicesfunctionscontinuePaymentSystemsResourcePoolingTransferResourcesFundsInflowsFundsOutflowsManageRiskManageIncentiveProblemsPriceInformation•Facilitateexchangeforgoods&services•Gatherfundsforlargeresourceneeds•Lendingandinvesting•Insuring,diversifyingandhedging•Incentfundsavailability•Supportefficientmarkets4Industry-wideChangeRequiresBCAssistanceBCServices•ProcessIntegration•MarketSelection•RevenueEnhancement•Process&ChannelAlignment•Efficiency•BusinessSelectionChange•Regulation•CustomerValue•CapitalEfficiency5ChangeIsEvidentWorldwide•CreditSuisse•cut5,000jobs•consolidateback-officeoperations•trimprivatebanking•stockpricerise11%•Japan•sweepingFinancialregulationreform•“AWesternstylefinancialsystem....demandingmuchhigherreturnsfromCorporateJapan”6ChangeIsEvidentWorldwide•DeutscheBank•reducedstaff10,000inthreeyears•invested$730millioninnewhiresandtechnology•investsinGermany’s#5,BayerischeVereinsbank•threatensAllianzininsurance•Asianinvestmentbankingexpansioninto17countries•Columbia•privatizeFinancialServicescompanies•enhancecompetitionandpromotescaleeconomies7ChangeIsEvidentWorldwide•U.S.insurance•CharlesSchwabsellsuniversallife•bankssell20%ofallannuities•quotesviainternet•commission-freeproductsfromdiscountbrokers•Portugal•privatization•consolidate50%oftopbanks•reducecoststructure,streamlineoperations8Companiesmanagecomplexdecisionswithlimitedexperienceandtools.•cost&riskcontrolfocusProcessImprovementBusinessRedefinitionCustomerValuePropositionLargeSmallSourcesofValueSizeofOpportunityMarketEvolutionAdvancedBasicMarketCompetitiveness•Customersatisfactionw/costandrevenuebenefits•Reassesssegmentationandalignment•Redefineobjectives,productsandoperations9“Missioncriticalchangedemandsskilledconsultants,withdeepserviceexperienceandindustryknowledgetoensuresolutionscanbeimplemented.”10LeveragingexistingskillsshouldbeourfirstactionHighLargePractice’sIndustryExpereincePracticeAreaMarketLowSmallJointVenture-ExporterR&DExporterJointVenture-ImporterFacilitator11WeHaveUnlimitedGrowthPotential•1995estimateforUSDepositoryInstitutionNon-technologyConsultingMarketapproaches$1.2billion.•WorldwideFinancialServicesConsultingOpportunitiesequal$???billionSmallMediumLargeMarketAAFeesAAShareofUSDepositoryNon-technologyConsultingMarketMarketSegmentIllustrative12SomepracticeshavebeguntheirmarketandskillassessmentsIIIIIIIVHILOWLOWHIPerformanceMeasuresCustomerSatisfactionOrganizationCapabilityRegulatoryRiskImproveBusinessOperationsLitigationConsultingTechnologyChangeImplementationStrategy/PlanningAA’sCapabilityIndustryNeeds(valuebased)13JoanWucherKingEMEIAFinancialMarketsIssuesandTrends14EMEIAInsuranceNetFeesAudit/TaxServices$32,038$42,053$0$10,000$20,000$30,000$40,000$50,0001996199531%0%20%40%60%80%100%NETFEES(000’s)GROWTH($10,015)15EMEIAFinancialMarkets*NetFeesAttestvs.Non-AttestServicesAttestNon-Attest$140,811$158,105$29,844$41,885$0$36,000$72,000$108,000$144,000$180,000At...